Federal Reserve Bank of Cleveland:

http://www.clevelandfed.org

John B. Carlson

Vice President

John Carlson is a vice president in the Research Department at the Federal

Reserve Bank of Cleveland. In addition to conducting economic research, he

oversees the department’s publications and its support functions. His research

interests include monetary policy, money demand, models of learning, and asset

pricing.

Public Pensions Under Stress

Public Finances: Shining Light on a Dark Corner

The financial crisis has made it all too clear that

regulators failed to see into the dark corners of the financial system. With

that in mind, the Federal Reserve Banks of Cleveland and Atlanta have formed a

Financial Monitoring Team to study pension funds and municipal finance with an

eye toward implications for the wider economy and financial system. What

concerns should we have? In this article and other articles from this spring

issue of Forefront, we explain where risks could be building and how

reforms might help forestall their impact on the broader economy and financial

system.

Since 2007, state and local governments have been caught in a perfect storm.

The confluence of the severe recession and the collapse of the housing bubble

dramatically slashed tax revenues. Although some revenue sources have rebounded

with the economy, the decline continues for others. Property values, a major

source of funding for local governments, remain especially depressed.

The toll has been particularly heavy on public pensions, whose troubles with

chronic underfunding predate the financial crisis. By one estimate, the nation’s

126 largest public pensions were underfunded by at least $800 billion in 2010.

By another, 54 percent of the country’s state and local plans will have

exhausted their funds as early as 2034.

It now seems inevitable that sacrifices will be required from current

employees, employers, and in some cases, retirees. What remains unclear is the

extent to which changes in future investment returns and pension plan designs

can close the funding gap.

On that count, one key question is this: Without strong remedies, at what

point would pension plans run out of money, leaving financially impaired state

and local governments on the hook? That question is not quite settled.

The answer hinges on complex economic and legal questions. The potential

implications of adding financial stress to already overburdened state and local

governments are all too clear. Up to this point, the consequences of local

pension plan insolvencies—though they inflict hardship on citizens—have been

isolated enough not to become epidemic.

How it all shakes out depends on the success of future reform efforts, not to

mention the investment returns on pension-fund portfolios.

The Scope of the Problem

First, a little background on pensions: About 80 percent of public pensions

are defined-benefit plans, meaning that the plan’s sponsor promises to

pay a specified income that is predetermined by years of service, final average

salary, and other factors. To fund the promised income, both the employee and

employer typically contribute to a pension trust. The trust invests these

payments in a portfolio of assets whose returns are expected to pay the lion’s

share of the benefit obligation.

Unfortunately, these expectations are not always met. Historically, public

pension plans have invested a large share of funds in stocks, which have offered

relatively high returns when averaged over long periods. Since the stock

market’s peak in 2000, however, equity returns have been sharply lower than

expected. As a consequence, the value of assets held in public pension trusts

has not kept pace with the growing promises the plans have made, leaving them

substantially underfunded.

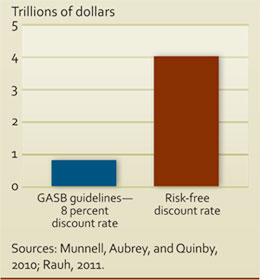

How far under is a matter of debate. According to the funding-status measure

prescribed by the Government Accounting Standards Board (GASB), the largest 126

pension plans were underfunded by around $800 billion in 2010. On the other

hand, some critics of GASB’s accounting methods estimate the aggregate pension

fund shortfall to be as much as $4 trillion. (See sidebar, “The Widely Ranging

Estimates of Pension Underfunding.”)

Embedded in those aggregate estimates are individual plans’ funding

ratios—the amount of assets held relative to the amount deemed necessary to pay

for a fund’s promised retirement packages. The funding ratio, however, does not

tell the whole story of a plan’s sustainability. It does not take account of

potential supplemental contributions that could help restore a plan to fully

funded status over some reasonable period.

A recent study by the Center for Retirement Research argues that judging the

adequacy of pension funding requires more than looking at a snapshot of the

funding ratio. A key issue is whether the sponsor has a funding plan and is

sticking to it. Under GASB rules, plan sponsors must report an annual

required contribution (ARC). Effectively, this is the annual amount a plan

sponsor would have to pay to eliminate any shortfall over a period of 30

years.

Although public pension plans’ annual reports must publish the percentage of

ARC payments they are making, not all states legally enforce such payments.

Since 2008, the average share of ARC paid has declined from 92 percent to 87

percent, according to the Center for Retirement Research, even though the same

payments as a percentage of payroll have actually increased.

Most state budgets have been under too much stress to make full ARC payments

voluntarily. Without mandatory ARC payments, the funding status of many pensions

will continue to deteriorate unless reforms increase employee contributions or

reduce benefits.

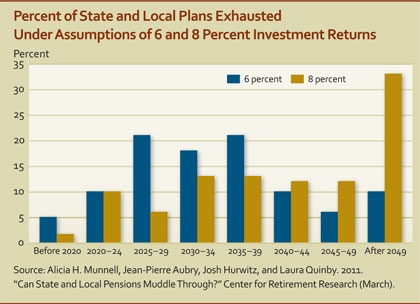

Estimating Plan Exhaustion Dates

The question then becomes how much time a plan has before it runs out of

money—the fund’s exhaustion date. A pension plan with a 60 percent funding

ratio, for example, may not run out of funds for 12 years. This stretch of time

would give this plan’s administrators some breathing room to implement necessary

reforms.

How much breathing room do the more severely underfunded plans have? One

study estimated exhaustion dates for the 126 largest pension plans, assuming the

plans are ongoing. Simply put, this means that employers and employees continue

to make contributions while benefits are paid out of the trust fund. Of course,

the exhaustion date also depends on investment returns on assets. The study

considered funding situations for returns of both 6 percent and 8 percent. Its

results show that although several plans will become insolvent in the next

decade, most would have some time to work out their difficulties (see

figure above).

Other estimates paint a bleaker picture. Joshua Rauh, Northwestern University

professor, finds that seven states would run out of money by 2020, and 30 more

would run out in the following decade, even assuming 8 percent investment

returns. Unlike the study mentioned earlier, Rauh assumes that employers make

only enough contributions to the pension funds to pay for the present value of

newly accrued benefits, and no more. On the other hand, a recent GAO study

concludes that Rauh’s projected exhaustion dates are not a realistic estimate of

when the funds might actually run out of money.

The Urgency of Pension Reform

If there is any hope that future investment returns will offset losses

following the financial crisis, it is slim indeed. Most plan sponsors recognize

this and have supported reforms that increase new employees’ contributions and

reduce their future benefits. Between 2008 and 2011, the National Conference of

State Legislatures counted 40 states that have implemented pension reforms.

But most of these changes have only a limited effect on plan funding. Until

recently, few states have attempted to alter benefits or contribution levels of

vested employees or retirees, which could have a far greater positive impact on

pension funding. Although some state legislatures have passed reforms that were

upheld in the courts, the fate of other efforts remains to be decided by the

courts. (See related article, “Navigating

the Legal Landscape for Public Pension Reform.”)

When funding ratios fall, the amount of cash generated by interest and

dividends from investments declines relative to the amount needed to pay

benefits. Without sufficient contributions to offset the lower cash flow from

investments, the process becomes self-reinforcing—that is, assets must be sold

to pay benefits, further reducing the cash generated by investments. This

becomes especially problematic when the funding ratio falls below 50

percent.

For example, the Rhode Island Employee Retirement System recently recognized

that its funding process could not be sustained without urgent action. In late

2011, the state legislature responded with sweeping pension reforms that passed

by an overwhelming bipartisan majority. Under the new law, current employees’

benefits will be frozen, modified, or even reduced, and retirees’ cost-of-living

adjustments will be suspended until the funding ratio improves enough to satisfy

sustainability conditions. Whether these actions will be sufficient remains to

be seen, especially since they will probably be challenged in the courts.

Is a Liquidity Crisis Imminent?

At this point, it seems unlikely that any major pension fund will run out of

cash in the next few years, barring a general worsening of economic and

financial conditions. Indeed, increased public attention on the underfunding

problem has motivated pension plan sponsors to work with state legislators to

implement substantive reforms.

But we are not out of the woods yet. Many funds will require significant

reforms to reduce underfunding levels, with painful new contributions from

employers and employees. Over the long term, a stronger, steadier economy would

help a lot by supporting higher asset returns. Meanwhile, an imminent collapse

of several large funds, accompanied by a shock to the financial system, remains

improbable—though not impossible.

Over the longer term, the current low-interest-rate environment may be cause

for concern. Fund managers will struggle to achieve 8 percent yields without

shifting their portfolio composition toward higher-yielding assets, which are

inherently riskier. Managers’ “reach for yield,” if practiced widely, would make

pension plan sustainability particularly vulnerable to another negative shock to

equity prices.

Another concern is that some states’ legal protections may be too strong to

give reforms enough time and flexibility to put plans on sustainable paths. In

that case, states would ultimately be on the hook for covering pension benefits

out of general revenues. This scenario, by creating crisis conditions in those

states, could stress economic conditions more generally. But we have by no means

reached that point yet.